March 30, 2025

11 min

·

June 26, 2024

As a small business owner operating in the B2B market, you understand the significance of the B2B payment procedure. However, the process is brimmed with obstacles, ranging from accurately matching invoices with payments to getting payments on schedule.

How do you choose the best payment method that fits your business model? How do you preserve unmatched efficiency while minimizing manual processes and errors?

The emergence of new technologies and digital solutions has paved the way for greater productivity and payment security. So, the world of business-to-business payments has seen significant changes recently, requiring you to adapt to them.

We’re here to help. We’ve put together this comprehensive guide to lead you through every step of the B2B payment process. Read on!

Check out our best invoicing app for tradies. Try the top app for tracking client payments today!

Business-to-business, or B2B, payments are defined as the exchange of funds (money expressed in local currency) for goods or services between a buyer and a supplier.

Depending on the terms of the contract signed by the vendor and the customer, B2B payments may be:

Compared to business-to-consumer, or B2C, payments, business-to-business (B2B) payments are more complicated and time-consuming. The approval and settlement of B2B payments might take several days or weeks. On the other hand, B2C payment processing usually settles the transaction immediately.

As B2B payments differ from B2C payments, small and medium-sized businesses should understand their peculiarities to choose the proper payment methods and processes. Here are their main differences:

Manage invoices, quotes, purchase orders, and delivery notes effortlessly with Billdu. Simplify your invoicing process—try Billdu today!

Payment types used in business-to-business transactions are diverse and have their own benefits and drawbacks. Understanding these can help small businesses choose the best approach to simplify their financial processes.

Thanks to advancements in fintech and payment processing, as well as the growth of eCommerce, B2B payment solutions have expanded dramatically in the last few years. Take tools like CPQ Salesforce or Billdu as an example.

They can quickly and accurately generate quotes for orders, streamlining sales transactions depending on the chosen payment method. Billdu, in particular, lets companies configure, price, and quote services and products, accommodating various payment methods to optimize their financial processes.

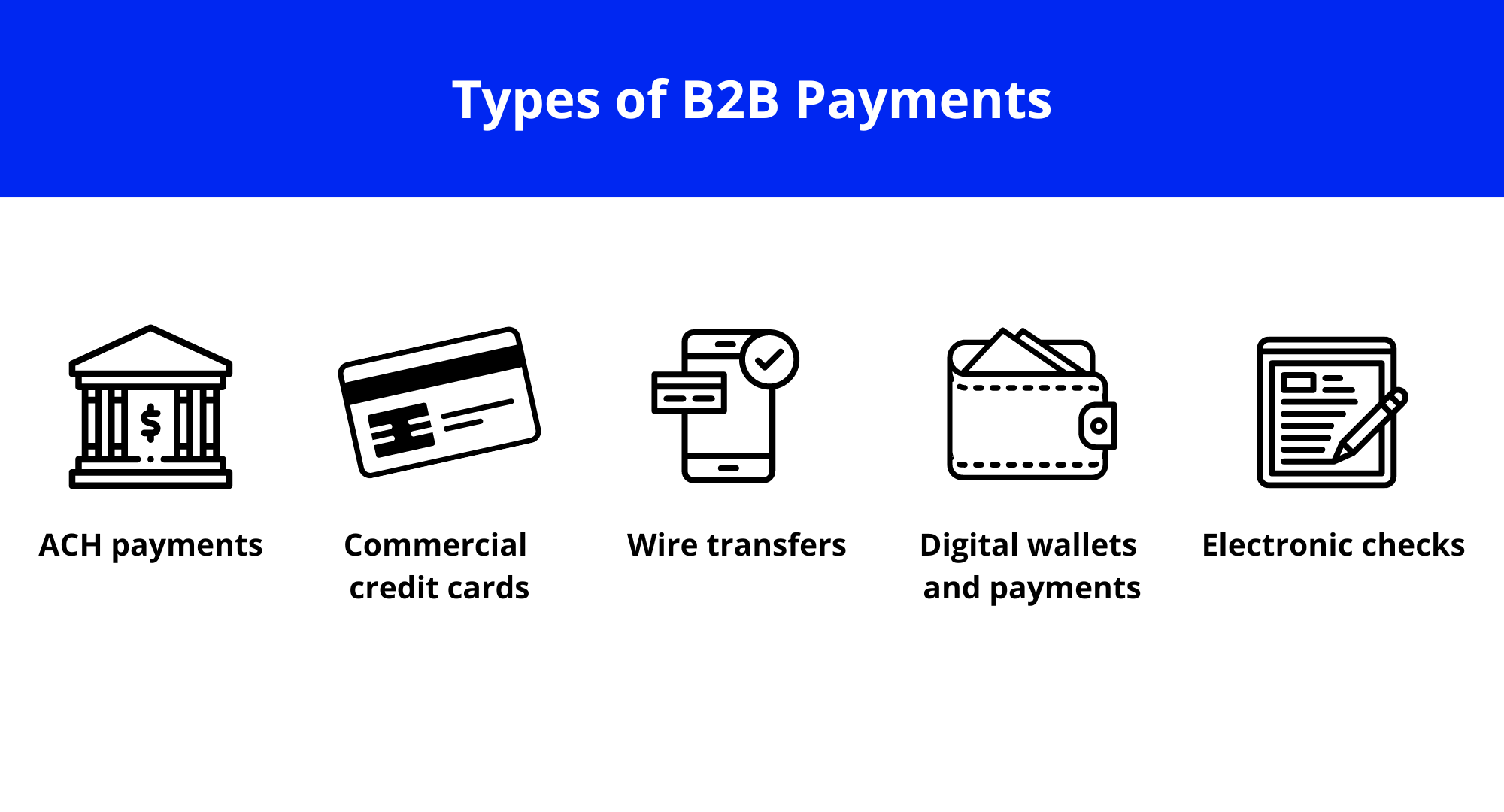

Paper checks and automated clearing house (ACH) transfers continue to be the most popular B2B payment methods as of 2024. However, there are numerous other cutting-edge techniques facilitating B2B payments, including:

Let’s explore these B2B payment methods, their advantages, disadvantages, and real-world applications.

The first option to transfer money in the US is through ACH payments. Due to their affordability, ease of use, and highest level of security, ACH payments are a widely acknowledged B2B payment option.

This method implies that electronic payments move between two parties using a routing number and bank accounts.

Few people need to communicate with one another during this procedure, so there is little friction. These are secure transactions and usually don’t cost the buyer or seller anything extra.

Pros:

Cons:

Wire transfers represent electronic payments sent from a buyer to your bank account. Businesses can direct funds via a financial network, so this payment method is typically faster than an ACH transfer, enabling real-time payments.

The most extended wire transfer takes up to one business day, while most are completed in a few hours. International bank transfers may require additional time and payment processing costs, depending on the service provider.

Wire transfers are among the less popular B2B payment options. Nevertheless, they make up a sizable portion of the B2B payment volume (per transaction) due to their popularity in making expensive payments to foreign parties.

Pros:

Cons:

Plastic remains among the most widely used payment options for many buyers, be it individuals or businesses. Credit card payments (employing Visa, Mastercard, American Express, and Discover) imply processing fees, making them one of the most costly ways for the supplier to accept payments.

Still, not supporting credit card payments online can result in a possible loss of business. That’s why most entities are ready to sacrifice short-term financial savings to retain clients. Companies can lower these expenses by implementing strategies like credit card surcharges.

Pros:

Cons:

Juniper Research predicts that by 2026, more than 60% of people will be using digital wallets. What are they? These are solutions that allow for instant payments from consumers’ devices.

Digital payment services come in many forms, such as Venmo, Apple Pay, Google Pay, PayPal, and others. These systems enable money to move electronically between accounts.

Even though the bank accounts are linked, the transfer usually happens between two entities rather than directly accessing the accounts.

Digital wallets and online payment systems offer extra features like note-adding and tracking capabilities, so some customers choose them instead of physical wallets. Another appealing feature is the additional ease of making transactions from a smartphone.

Pros:

Cons:

Companies continue to pay other businesses with paper checks despite a notable drop over the last ten years. Modern customers seek convenience and value speed. But it’s not always the case in the business world.

It’s data privacy that matters. Paper checks cause more security concerns than other forms of payments, so they may not be the best option.

Unlike digital payments, they lack encryption, two-factor authentication, real-time fraud monitoring, and other security measures. If they fall into the wrong hands, checks can expose sensitive information.

At the same time, checks remain quite popular B2B payment solutions as they provide a physical payment record, leave a clear audit trail, and help a brand manage cash flow and inventory more effectively. Digital payments aren’t always able to accomplish this.

The reasons to consider this payment method are as follows:

Pros:

Cons:

While some may be using paper checks to pay other businesses, an e-check, or electronic check, offers a modern take on traditional payment methods.

Also known as a direct debit, an e-check contains the same information as its paper counterpart. However, as the name implies, e-check transactions are handled electronically.

Electronic checks are quicker and less expensive to process than credit card transactions. Because of this, they can be appealing and handy for both buyers and sellers.

Pros:

Cons:

Ensure timely payments with Billdu invoicing software. Start using Billdu today and streamline your invoicing process!

The field of B2B payments is evolving along with technology. Let’s examine the main trends in B2B payments that shape the industry, from the reduction of operations with paper checks to the emergence of new B2B payment methods like digital B2B payment solutions.

During the past few decades, the use of paper checks has decreased due to the advantages of credit cards, digital payment platforms, and other alternative payment methods.

The 2022 AFP® Electronic Payments Report states that only 33% of businesses made B2B payments in 2022 via checks, compared to almost 80% of companies that made similar payments with checks in 2004.

As paper checks become less common, it’s crucial for small businesses to stay current with other widely used B2B payment methods.

For example, companies like GoCardless, with its Direct Debit feature, Square, and Stripe offer innovative online invoicing, recurring billing, and real-time payment tracking tools. These platforms simplify the transaction process and provide enhanced security measures to protect sensitive financial information.

Mobile devices are replacing desktops in the B2C sector when it comes to shopping. This trend has also appeared in the B2B sphere. More and more businesses prefer to buy from smartphones. That’s why you need to streamline mobile purchases and introduce services like PayPal, Zelle, and Venmo.

This rule is crucial if you work in sectors like wholesale distribution, food supply, or field services, where transactions can occur on the go. Thanks to a mobile platform’s autonomy, you can enhance customer experience in these cases.

Real-time B2B payment processing is another concept that is gaining traction. Similar to same-day ACH, many countries are developing and planning immediate (or real-time) payment systems and infrastructures.

Businesses need payment processing that is always on, secure, easy to use, quick, and convenient. This demand is encouraging further upheaval and innovation in the payments sector.

Another notable trend originated from consumer markets: buy-now, pay-later (BNPL) solutions, or split (deferred) payments. BNPL offers flexible payment terms for business owners on both sides of deals.

BNPL arrangements allow businesses to receive goods or services immediately but pay later, usually without interest, if they comply with the agreed terms. This contributes to customer satisfaction, allowing buyers to manage their finances more effectively without immediate financial strain.

Klarna and Afterpay are examples of payment processing providers. Initially designed for B2C, they have extended their services to cater to B2B payments. This trend is particularly appealing in industries where upfront costs can be prohibitive. It enables smaller businesses to compete more effectively and manage inventory without significant capital outlay.

The economy has been highly volatile since early 2020. Desperate times, as they say, require desperate means, and businesses are experiencing an exponential rise in the likelihood of financial crimes like invoice fraud. As such, the security measures of digital B2B payment methods are increasingly valuable.

Electronic payments come with key features like encryption and transaction monitoring, which can significantly reduce the risk of fraud. Businesses also leverage advanced technologies like blockchain for secure, transparent B2B payments. For instance, IBM’s Blockchain World Wire offers a network for cross-border payments, ensuring greater protection.

Effective and efficient payment management is extremely important to operating a profitable B2B company. Businesses need to take into account a variety of factors related to B2B payments, including:

A few of the common challenges in B2B payments are as follows:

Reconciling numerous invoices and processing payment data manually might be time-consuming and inconvenient. For instance, clearing checks can take several days or even weeks, while processing wire transfers can take several days.

Payment data is frequently missing, and back-office personnel have trouble putting it all together. Electronic payments, however, streamline this, significantly reducing wait times.

Payment charge issues may arise because of the high frequency and high value of certain B2B payments. Regularly utilizing wire transfers or bank payments can eat into profits.

Furthermore, B2B payments frequently involve several currencies, raising complexity and expenses. Electronic payment platforms often offer lower fees while also minimizing manual effort.

Due to the significant amount of money involved, B2B payments have always been lucrative targets for fraudsters. Plus, because of their intricacy, malicious behavior can be challenging to identify.

As there are few permission controls for each operation, there is a substantial danger of fraud. It’s incredibly prevalent among paper-based and manual payment methods. If a fraudulent payment is processed, a company may be responsible for the money, the cost of the items sold, and any compensations or penalties imposed during the chargeback procedure.

Solution: Opt for digital solutions that offer advanced security features.

There are numerous reasons for late payments. Manual processes, poor visibility, and delays in fund transfers are among the widespread factors affecting both accounts receivable and payable.

Automation, self-service portals, and electronic invoicing can ensure timely payments, reduce the need for manual data entry or cash application, and minimize keystroke mistakes.

This challenge is primarily relevant to traditional B2B payment methods. Limited flexibility, manual effort, and disconnected systems can hinder effective communication between departments and with external partners.

But there is a remedy. Integrated payment systems can enhance collaboration and customer relationships by providing real-time data and improving visibility.

If you’re looking for a comprehensive solution for small businesses, pay attention to Billdu. This invoicing software can tackle these B2B payment challenges, supports various payment methods, and lets you manage payments online. Key features include:

As many of Billdu’s clients highlight, the software is user-friendly, professional, and time-saving. Users across various sectors have found Billdu invaluable. For example, the platform’s ease of use, especially for startups, simplifies payment and invoice tracking, directly addressing the need for efficient payment acceptance and better cash flow management within the B2B payment gateway landscape.

Stay on top of all your payments with Billdu. Simplify your financial management today! Check out our affordable price plans.

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy