January 10, 2025

10 min

·

January 22, 2025

Running a business means keeping track of many details — especially financial data.

And while managing business finances may not always be the most exciting task, it’s one of the most important. Without proper bookkeeping, your business could face serious challenges down the road.

But, many small business owners put off bookkeeping because it can feel overwhelming.

The good news is it doesn’t have to be complicated.

In this guide, we’ll explain the basics of bookkeeping, why they’re important for your success, and how you can get started today.

Bookkeeping is an accounting process business owners use to record and organize financial transactions. The goal is to track business income, expenses, and overall financial health.

Some practical examples of bookkeeping include:

Simplify your billing with invoicing software for entrepreneurs! Create professional invoices quickly and get paid faster—try it for free today!

Free 30-day trialNo credit card requiredCancel anytime

Free 30-day trialNo credit card requiredCancel anytime

Bookkeeping is important because it helps you see how much money your business is making and spending. It makes tax filing more manageable and prevents you from overlooking important details.

Proper bookkeeping can also help you grow your business by clearly viewing your financial health. With these insights, you can spot trends, manage cash flow, and make wise decisions to boost profits.

For instance, you can check to make sure you’re not overspending. And if you are, you can identify areas to cut costs.

You can also see where the bulk of your revenue is coming from, allowing you to allocate more time and resources to those areas.

Organized finances also make it easier to apply for loans or attract investors since they’ll see that you’re running a well-managed business. This is important if you plan on selling your business one day — or if you’d like to bring in partners.

Here are some essential bookkeeping terms you need to know.

Feel free to print the following chart and pin it to your bulletin board or in a notebook on your desk.

Term | Definition | Example |

Assets | The resources your business owns (i.e., cash, equipment, inventory). | Your store’s shoe and purse inventory. Or your work laptop. |

Liabilities | Debts or obligations your business owes — like loans or accounts payable. | A small business loan. Or any bills you owe to suppliers. |

Equity | Your share of the business after subtracting liabilities from assets. | If your business is worth $10,000 and you owe $4,000, your equity is $6,000. |

Income (Revenue) | The money you earn from sales or services. | The money you earn from selling products in your online store. |

Expenses | The costs you incur when running your business include rent, utilities, and supplies. | You pay for electricity or restock inventory for your shop. |

Accounts receivable | Money customers owe you. | A customer buys something on credit and promises to pay $100 next week. |

Accounts payable | This is the money your business owes to suppliers or vendors. | You owe $200 to your supplier for new inventory. |

General ledger | A master record with all of your financial transactions. | You use a spreadsheet or software app to record every sale, payment, and expense. |

Trial balance | A summary of all ledger accounts to check for errors. | To keep accurate records, you check if total debits match total credits. |

Cash flow | The money that moves in and out of your business. | Cash comes in from sales, and cash goes out for rent payments or inventory purchases. |

Depreciation | The decrease in value of assets over time. | Your delivery van’s value decreases as it gets older and you use it more. |

Balance sheet | A snapshot of your business’ financial position (assets, liabilities, equity) at a specific point in time. | This month’s report shows your business currently has $10,000 in assets, $4,000 in liabilities, and $6,000 in equity. |

Profit and loss (P&L) | A report showing how much money your business made and spent over some time. | A monthly report shows your business made $5,000 in sales, spent $3,000 on expenses, and made $2,000 in profit. |

Bookkeeping uses systems to record your business transactions. However, each system type works a bit differently.

The main bookkeeping systems are:

So, which one should you pick?

Here’s what you need to know about each.

→ Accrual-based system: This system gives you a clearer picture of your business’ financial health. It tracks revenue and expenses when they occur, not just when you use cash.

This option is ideal if you offer credit to customers. Or have complex financial transactions.

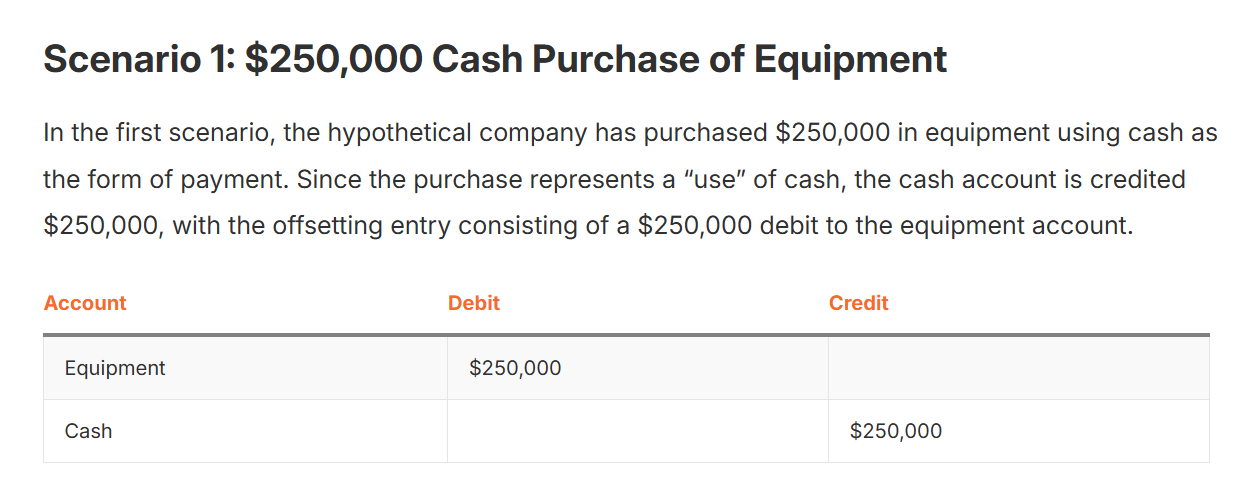

→ Double-entry system: This is a more thorough system. Every transaction is recorded in two places (debit and credit).

This system is a great option for a large or growing business.

Here’s a quick look at what this looks like for an equipment purchase:

→ Single-entry system: This simpler and quicker system is suitable for small businesses with fewer transactions. Cash-based businesses, like retail shops, use this bookkeeping system, where tracking every credit and debit isn’t necessary.

Choose this if you have minimal transactions or operate as a cash-based business.

→ Hybrid system: Combines aspects of both the single-entry and double-entry systems.

It is helpful if your business has mixed transaction types (some simple cash sales and some credit sales).

→ Cash-based system: This records transactions only when cash changes hands.

This system can be easier to track if you run a business where payments are always made immediately, like a coffee shop.

It depends on the complexity of your business. A single-entry or cash-based system might be enough if you’re starting small and only dealing with cash.

As your business grows or if you offer credit, you may need the accrual-based or double-entry system. Start simple and scale as needed.

Need a way to streamline and organize the process across departments?

Consider using an intranet software to access your bookkeeping system. (Make sure it’s integrated or linked.) This will give your team a secure, centralized hub to view financial records, track transactions, and collaborate on bookkeeping tasks.

Implement continuous security validation, along with regular backups and access controls, to ensure the safety of your intranet. This will protect your sensitive financial data from unauthorized access or tampering.

Let’s review some more tips you should keep in mind.

Speed up your clients’ payments with Billdu! Send professional invoices and automated payment reminders—try it for free today!

Free 30-day trialNo credit card requiredCancel anytime

Keep the following best practices in mind when managing your books.

Keep a detailed record of every transaction to understand your cash flow and spot areas for improvement.

Open a separate bank account for your business to avoid mixing personal and business transactions. This approach simplifies bookkeeping and tax filing.

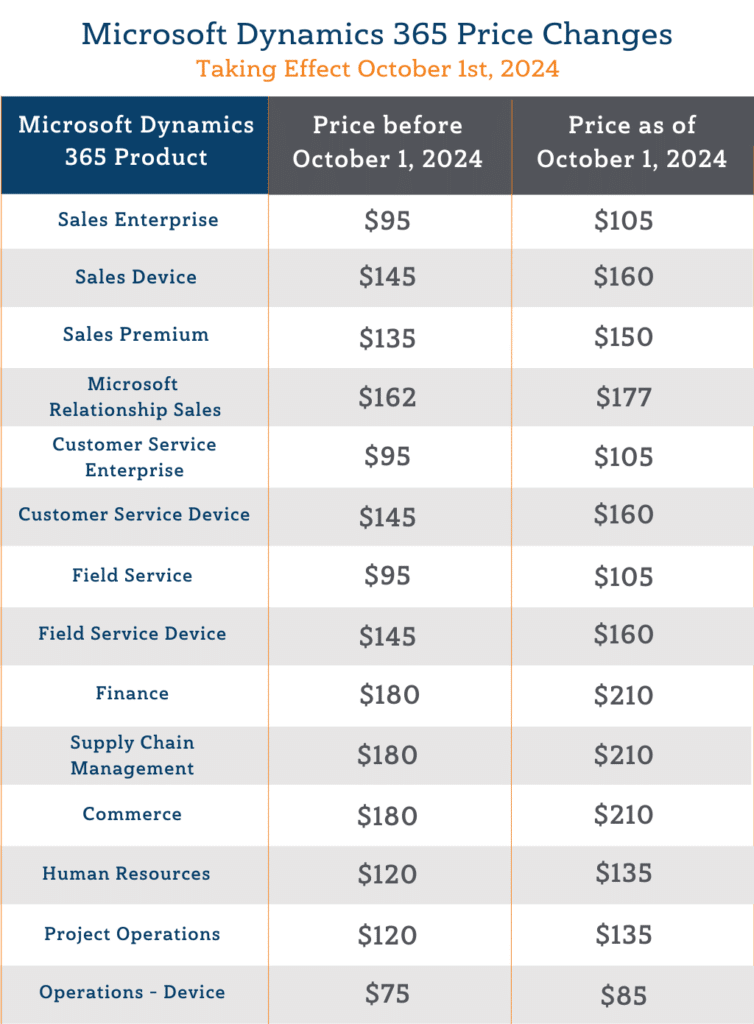

Regularly review your tech stack. Compare pricing plans and changes, like this breakdown of Microsoft Dynamics pricing, to make sure you’re not paying for more features than you need:

Consider downgrading to a free or mid-range plan.

Regularly assess your business expenses to find areas where you can cut costs — such as products or services you no longer use.

Plan ahead for taxes by setting aside a portion of your income regularly. (This prevents surprises during tax season and keeps your business finances on track.)

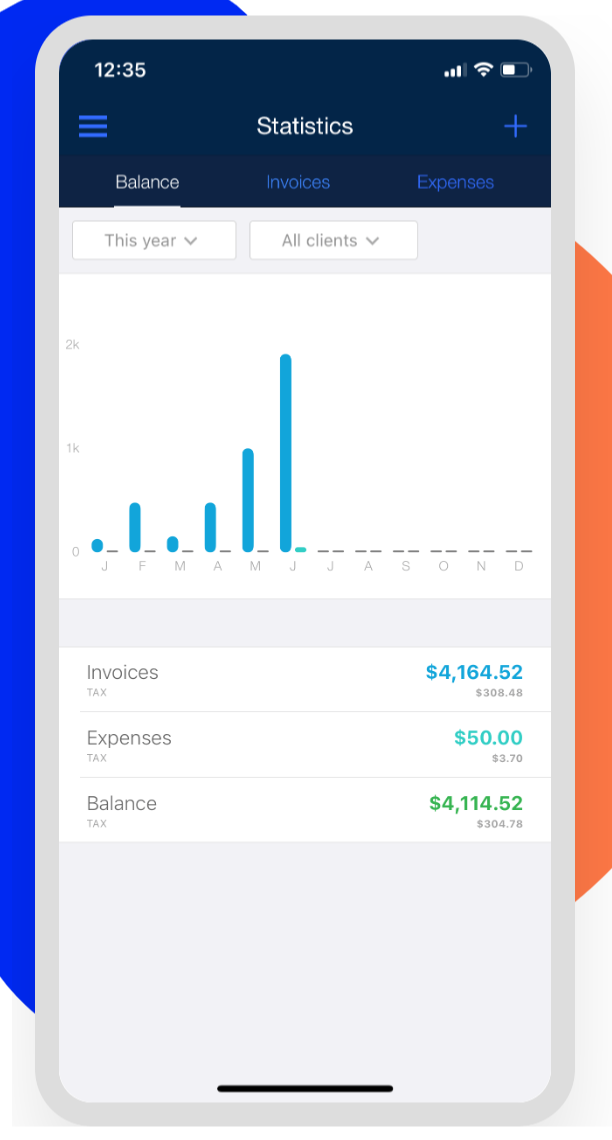

Review your profit and loss statements regularly. Identify profitable areas in your business and areas where you may need to cut costs. This is key to making data-driven financial decisions that increase revenue!

Ready to start the bookkeeping process?

Follow these six, straightforward steps.

The first step is to decide whether to use software or manual records. You can start with a manual system if you prefer a simple, hands-on approach. However, bookkeeping software like Xero is a great choice for efficiency and accuracy.

You can also integrate Billdu with it to automate key tasks like invoicing, expense tracking, and payment reminders. It lets you create professional invoices, record payments, and manage receipts digitally.

You can also use Billdu’s mobile app to manage your books on the go. (If you’re a freelancer or solopreneur, Billdu may be the only software you need!)

Pick a bookkeeping system that fits your business needs.

Remember …

A simple system like single-entry might work if you’re just starting out. However, a double-entry system might be a better fit if you want more detailed tracking.

Hybrid systems combine both, which means you’ll have flexibility.

Cash-based systems only track transactions when you use cash. And accrual-based records transactions when they’re earned or incurred — even if cash hasn’t changed hands yet.

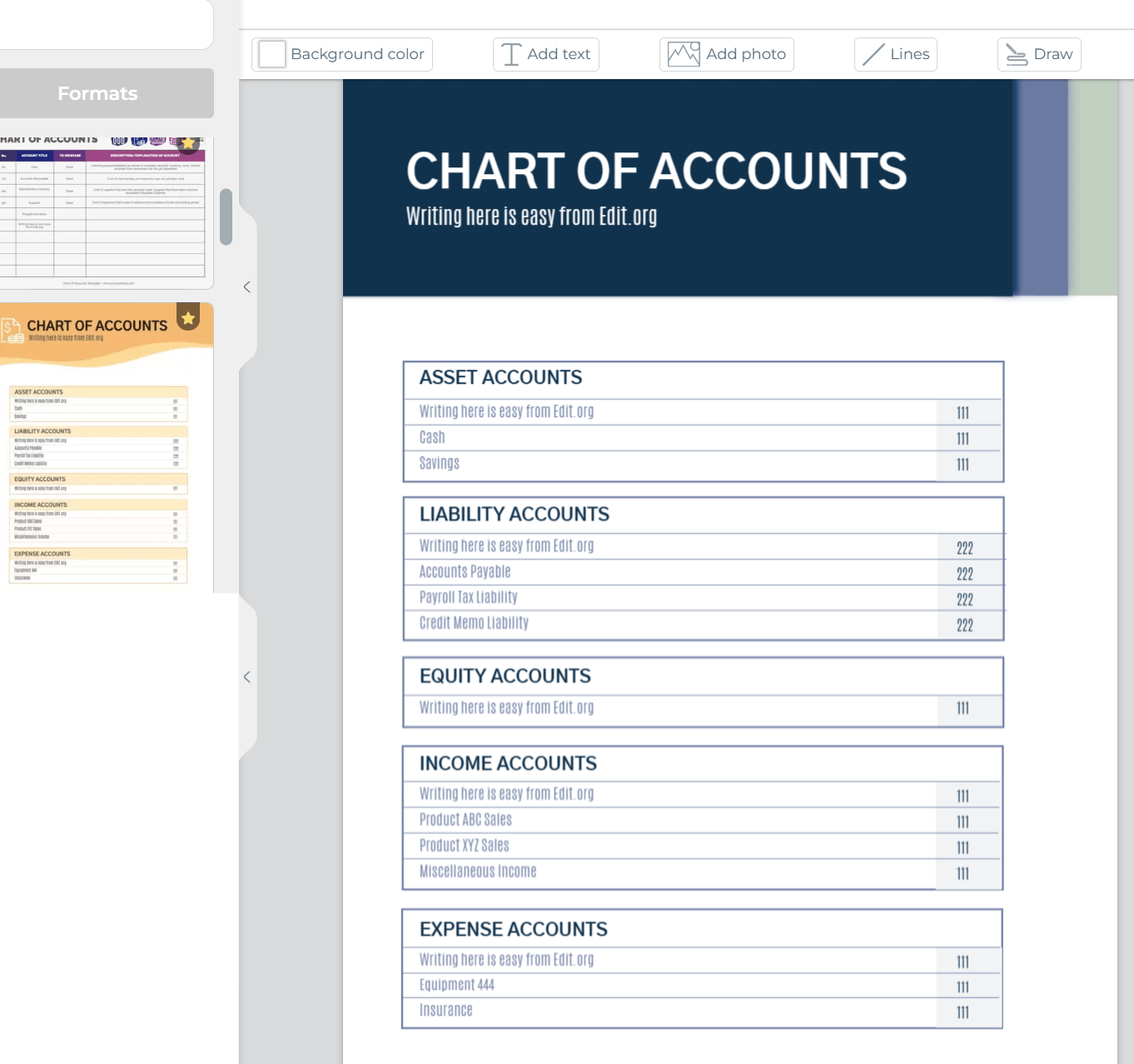

A chart of accounts is like a financial blueprint for your business. It categorizes transactions into specific groups: assets, liabilities, income, and expenses.

A structure like this helps you stay organized and makes financial reporting easier.

Take time to set it up correctly to avoid confusion later on.

Here’s a template to give you an idea of what it looks like:

Always keep your business and personal finances separate. This makes bookkeeping easier and prevents you from misplacing personal and business expenses.

Use a separate business bank account, and consider using a credit card just for business purchases. Fun fact: Most entrepreneurs (83%, specifically) used credit cards for their businesses in 2023!

Record every payment you receive and every expense you incur, including sales, bills, office supplies, and utility payments. The more detailed and consistent you are, the easier it is to see where your money’s coming from and going.

Regularly match your bank statements with your records.

This step helps you account for all transactions and spot errors or discrepancies.

Set a schedule (whether weekly or monthly) and stick to it to keep your books accurate and up to date.

When deciding between outsourcing your bookkeeping or handling it yourself, consider the pros and cons of each option.

For example, outsourcing offers expertise.

A professional bookkeeper can accurately handle your financial records, save time, and keep you compliant with tax laws. You won’t need to worry about mistakes, missed deadlines, or learning the ins and outs of accounting software.

However, it comes at a cost. And you’ll need to trust an external party with your sensitive financial information.

On the other hand, DIY bookkeeping can be a more budget-friendly choice.

The right software can help you manage your finances efficiently. This option gives you complete control over your records anenables you toou understand your business’s financial health firsthand.

The downside is it can be time-consuming and stressful if you don’t have any accounting experience. This can lead to mistakes or missed opportunities.

Basically …

If you have the time and inclination to learn, DIY bookkeeping might be the way to go.

But outsourcing might be the smarter option if your business is growing or you simply want peace of mind. When deciding, consider your budget, available time, and comfort level with numbers.

Automation SaaS tools can help simplify financial tracking for you and your bookkeeper.

For instance, try Billdu to automate your:

Bookkeeping is vital for any business.

It’s how you track your income and expenses and make smarter decisions about your financial future.

If you want to streamline your bookkeeping, tools like Billdu make it easier to manage invoices, track expenses, and generate financial reports. And with its flexibility, you can grow with it as your business evolves.

Stay on top of your financial health with solid bookkeeping practices and the right tools. Sign up for a free 30-day Billdu trial to simplify your bookkeeping now.

Advance your business with Billdu! Create professional invoices, send payment reminders, and manage your billing from just $4.99 a month.

Free 30-day trialNo credit card requiredCancel anytime

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy