March 25, 2025

11 min

·

March 13, 2025

You and your business are legally the same entity as a sole proprietor. Unlike corporations or LLCs, you don’t receive a traditional paycheck. And there’s no distinction between business and personal income. Instead, you take money from your business profits.

But paying yourself isn’t as simple as withdrawing money when needed.

Without the right strategy, your business could experience cash flow or underfunding problems or incur an unexpected tax bill.

Thankfully, we’ve compiled this handy overview to guide you through what you need to know.

We’ll cover withdrawals, cash flow, and tax planning so you can run a financially sound sole proprietorship.

Let’s take a look!

A sole proprietorship is the simplest business structure. However, it comes with financial responsibilities that differ from those of corporations or LLCs.

For instance, since there’s no legal separation between you and your business, all business income is considered personal income.

As a result, here are some real-world consequences you’ll experience:

You don’t receive a salary because there’s no formal payroll system. Instead, you take an owner’s draw — a direct transfer of funds from your business bank account to your personal bank account.

But without structured paychecks, you need to manage your finances strategically.

Head to the next section to learn how.

Get paid faster—because payment speed is everything in invoicing! Accept online payments with Billdu and turn invoices into cash in no time.

As a sole proprietor, you decide how much and when to pay yourself. To promote financial health, follow these best practices:

One of the best things you can do as a sole proprietor is to keep your business and personal finances separate. Open a business bank account to track income, pay expenses, and plan for taxes.

Instead of withdrawing funds randomly, consider a weekly, biweekly, or monthly draw that mimics a paycheck.

Doing this helps maintain consistency in your finances. It also prevents unnecessary withdrawals that could harm your business’ cash flow.

Ensure your business has enough funds to cover operational costs before withdrawing money for personal use. Regularly review your cash flow reports to see how much you can take without jeopardizing your business.

Set aside at least 25-30% of your income for taxes. And maintain an emergency fund for spontaneous business expenses.

(Ask your accountant for specific amounts.)

Calculate your average monthly business revenue and subtract your necessary expenses to determine how much to pay yourself.

Your expenses might include:

Once you have a clear picture of your profits, set a percentage or amount for your owner’s draw.

Withdraw what’s necessary for your personal expenses and reinvest the rest into your business. Remember to factor in taxes, too. This strategy supports your business’s future growth — and helps make sure you have enough to cover operating costs.

Here’s some math to crystallize this:

Let’s factor in a 30% tax reserve. And a $750 monthly deposit into your business emergency cash flow fund.

In this example, you can safely withdraw $3,800 and keep $750 in the business for cash flow. (You’re covering your taxes, paying yourself, and maintaining a buffer for your business!)

Let’s talk a little bit more about taxes in the next section.

Since your business income flows directly to your personal tax return, you must plan for taxes throughout the year.

This planning should include:

To stay compliant:

Consider opening a separate tax savings account and automatically transferring a percentage of every payment you receive. Having a separate account prevents you from accidentally spending money you’ll need for taxes later.

Figuring out how much to pay yourself can feel like a juggling act. Billdu makes the process so much easier. ☺️

With Billdu, you can:

Track income, cash flow, and expenses

See your transactions in one place to know what’s left over.

Billdu gives you a clear real-time financial overview of your income and expenses — so you always know what’s available to pay yourself.

Create and send invoices

Billdu lets you create professional invoices in minutes and send them directly to clients. You can also track when clients pay, so you know when you can withdraw money based on incoming payments.

Separate finances

Billdu lets you categorize your transactions to easily distinguish between business and personal expenses.

Plan for taxes

Estimate what you owe and set money aside so there are no surprises.

Billdu automatically tracks your expenses and generates reports that help you estimate your tax obligations. You can also export the data for your accountant.

Check profitability

Billdu offers detailed reports that show your business’s income, expenses, and profits. These help you determine whether your business is doing well enough to increase your pay or whether you need to reinvest to keep growing.

To further streamline your financial processes, consider integrating a QR Code Generator into your workflow. QR codes can simplify payments, making it easier for clients to pay you, which in turn helps you manage your cash flow and pay yourself more efficiently.

➔ Billdu allows you to manage your finances, avoid cash flow issues, and pay yourself confidently.

Get paid faster and simplify your invoicing with Billdu! Try Billdu free for 30 days, then continue for just $4.99 a month.

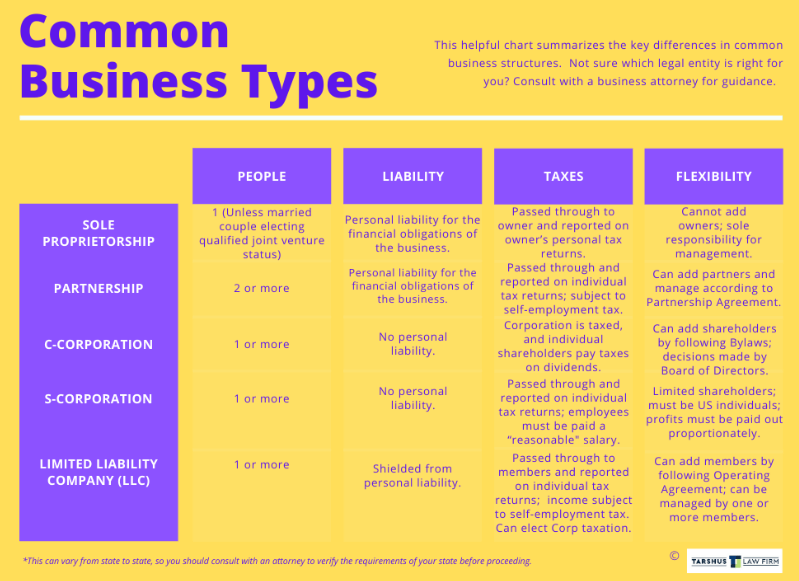

As your business grows, it may be in your best interest to transition to a different business structure since each offers different tax benefits and liability protection.

(How you pay yourself will change depending on your business entity.)

For instance, with:

Here’s a more in-depth chart that breaks down these options and more:

Electing S Corp status can help minimize self-employment tax for sole proprietors earning a high income.

However, this requires additional administrative work, such as payroll and filing corporate tax returns. To determine the best structure for your situation, consult with a tax professional and consider which legal tools can streamline the transition.

Head to the next section if you’d like to take our quiz on choosing a business entity.

Take the following quiz to see which business structure might best fit your goals as you scale.

(Final results are at the end of the quiz!)

A) I want to make all decisions myself without consulting others.

B) I’m okay with sharing decision-making power with others if needed.

What it means for your structure:

A) Sole Proprietorship or Single-Member LLC (SMLLC) might be your best bet since you’ll have complete control.

B) A multi-member LLC or partnership could work if you share your decision-making with others.

A) I’m comfortable being personally responsible for business debts and legal issues.

B) I’d prefer to limit my liability and protect my assets.

What it means for your structure:

A) Sole Proprietorship offers no liability protection. Meaning you’re personally responsible for business debts.

B) LLCs and S Corporations provide limited liability protection. They can shield personal assets from business-related debts.

A) I’m okay with taking profits as distributions (not salary).

B) I want a regular salary with clear tax withholding.

What it means for your structure:

A) For Single-Member LLCs or Multi-Member LLCs taxed as a partnership, you can take profits as distributions. These are taxed based on your share of the LLC’s income.

For LLCs taxed as S Corps, owners must take a reasonable salary through payroll (with tax withholding). They can take profits as distributions.

B) If you want to pay yourself a salary and reduce your self-employment tax burden, S Corporation status could be ideal. It allows salary payments in addition to distributions.

A) I prefer minimal administrative work and a more straightforward structure.

B) I’m willing to do additional paperwork for tax benefits and liability protection.

What it means for your structure:

A) Sole Proprietorships or Single-Member LLCs are the simplest structures, requiring minimal paperwork.

B) LLCs and S Corporations involve more paperwork — but offer benefits like limited liability and tax flexibility.

A) I expect my business income to be lower and don’t need tax-saving strategies.

B) I anticipate higher business income and want strategies to reduce taxes.

What it means for your structure:

A) A Sole Proprietorship or Single-Member LLC might be sufficient if you’re just starting and expect a lower income.

B) If your income grows, an S Corporation might be worth considering to reduce self-employment taxes. As an S Corp, you can pay yourself a reasonable salary and take additional profits as distributions (taxed at a lower rate).

A) I’m comfortable paying taxes based on my business income without overplanning.

B) I want to minimize my tax liability and plan ahead.

What it means for your structure:

A) Sole Proprietorships and Single-Member LLCs are taxed as personal income. Meaning you’ll pay self-employment taxes on all profits.

B) S Corporations allow you to pay yourself a salary and take distributions, which can help you save on self-employment taxes.

Mostly A’s: You might be best suited for a Sole Proprietorship or a Single-Member LLC. These structures offer simplicity and ease of control. (But don’t provide personal liability protection.)

Mostly B’s: Consider an LLC or S Corporation. These structures offer liability protection and tax flexibility — with an S Corporation providing a salary option to reduce self-employment taxes.

Friendly reminder: Consult a tax professional before choosing your business entity.

Paying yourself as a sole proprietor requires careful planning.

Separating your personal finances from the business finances, monitoring cash flow, and saving for taxes are essential for financial success.

Whether you continue operating as a sole proprietor or transition to an LLC or S Corp, structuring your payments promotes financial stability and supports long-term business growth.

Remember, Billdu is here for you! Sign up for a free 30-day free trial to see how much simpler financial management can be.

Free invoice generator? Invoicing has never been easier with Billdu! Try it free for 30 days and upgrade for just $4.99 a month.

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy