March 30, 2025

10 min

·

July 12, 2024

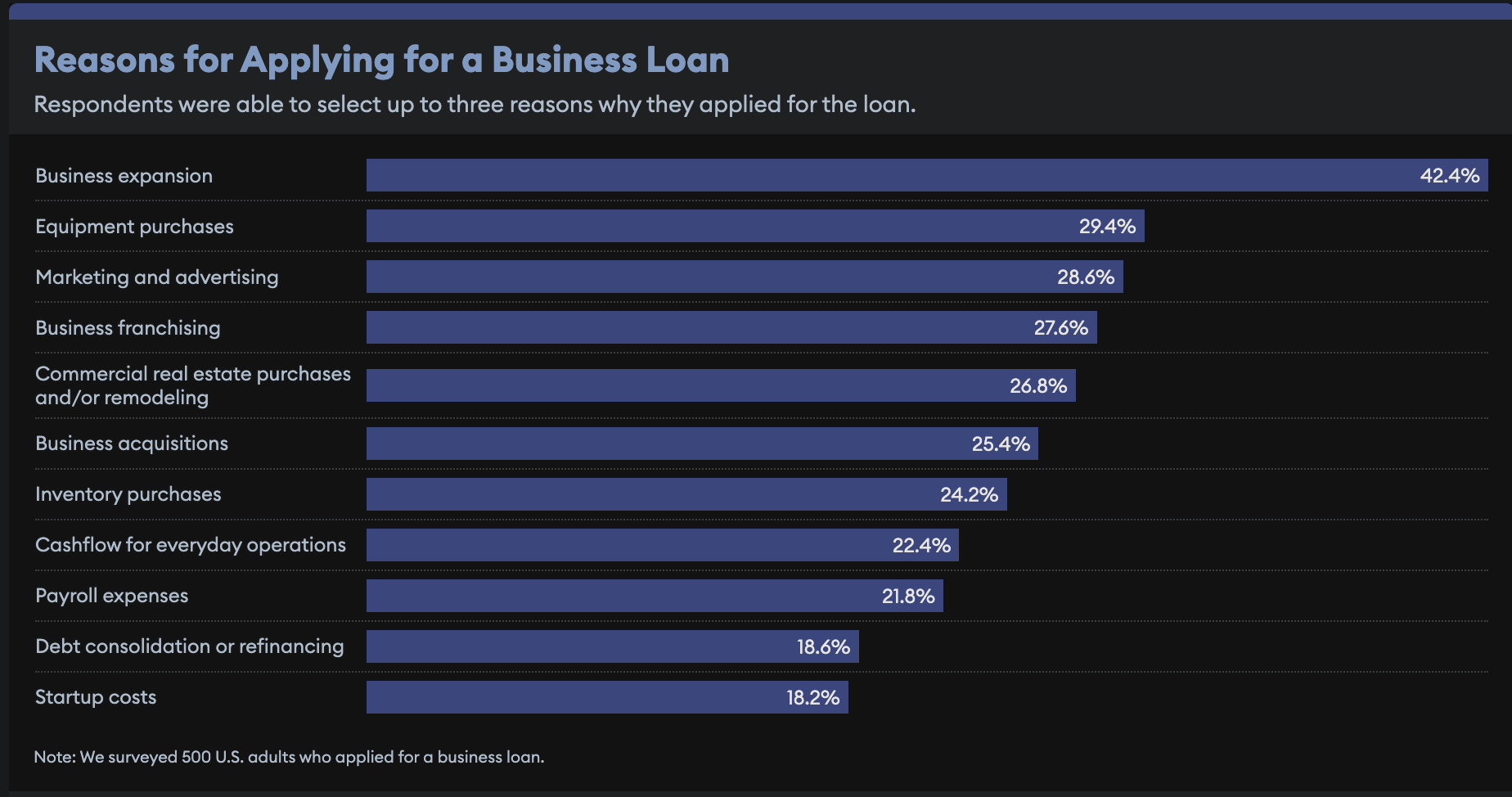

Business loans are crucial across all business stages—from startups and SMBs to established enterprises. According to the Forbes Advisory survey, business loans were the most common funding method for businesses in 2023.

The survey also shed light on the primary uses of these funds:

These loans specifically come from banks, credit unions, and online lenders. They all have different interest rates, repayment terms, and eligibility requirements.

If you’re a business owner wanting to expand your reach or seeking financial stability for your business, this guide is for you. We’ll talk about how business loans work, the process, what terms and conditions to keep in mind, and more.

Business loans are pivotal financial instruments designed to meet companies’ diverse capital needs. At its core, a business loan involves:

Borrowing a fixed amount of money from a financial institution or lender, which the borrower agrees to repay over a predetermined period, along with interest.

This financial leverage is crucial for businesses of all sizes as it enables them to:

For small enterprises, a business loan can be the lifeline that supports growth or helps bridge the gap during slow periods. These loans can fund inventory purchases, new technology, or even a physical expansion.

In contrast, large companies might utilize loans to finance major projects, acquire smaller businesses, or support large-scale research and development efforts.

The importance of business loans extends beyond the immediate infusion of cash. They also enable businesses to build credit, explore new opportunities, and remain competitive.

Easily manage your finances with Billdu’s invoicing software. Try it now and streamline your billing process today!

Business loans come in various forms to cater to different financial needs and circumstances. Here’s an overview of some of the most common types of business loans:

Term loans are straightforward, traditional types of loans where a business borrows a lump sum amount from a lender and agrees to pay it back over a set term with interest. These are suitable for companies looking to fund major investments like expanding facilities or making significant purchases.

The U.S. Small Business Administration (SBA) guarantees various loan programs to assist small businesses that might not qualify for traditional bank loans. SBA loan programs are crafted to address specific financial needs, ranging from property purchases to working capital. These include:

SBA 7(a) Loans: The most popular among SBA offerings, 7(a) loans offer up to $5 million, which can be used for working capital, expansion, and more. They are known for their flexibility in terms of usage.

SBA 504 Loans: Targeted at economic development, SBA 504 loans provide long-term, fixed-rate financing up to $5 million for significant assets like purchasing buildings or machinery.

SBA Microloans: Microloans are smaller loans up to $50,000 designed to help small businesses and specific non-profit childcare centers start and expand.

A business line of credit provides flexible access to funds up to a specific limit. This enables businesses to draw and use funds as needed. This makes it ideal for managing cash flow and unexpected expenses.

Equipment financing is a loan specifically for purchasing new or used equipment. Businesses can use the equipment as collateral for the loan, often with terms that match the expected life of the equipment.

Invoice financing allows businesses to borrow money against the amounts due from customers. It provides immediate cash flow based on outstanding invoices. This can be particularly useful for companies with longer invoice cycles.

Qualifying for a business loan often depends on meeting specific lender criteria. Understanding these requirements can help you better prepare your application and increase your chances of approval. Let’s explore the familiar qualifications:

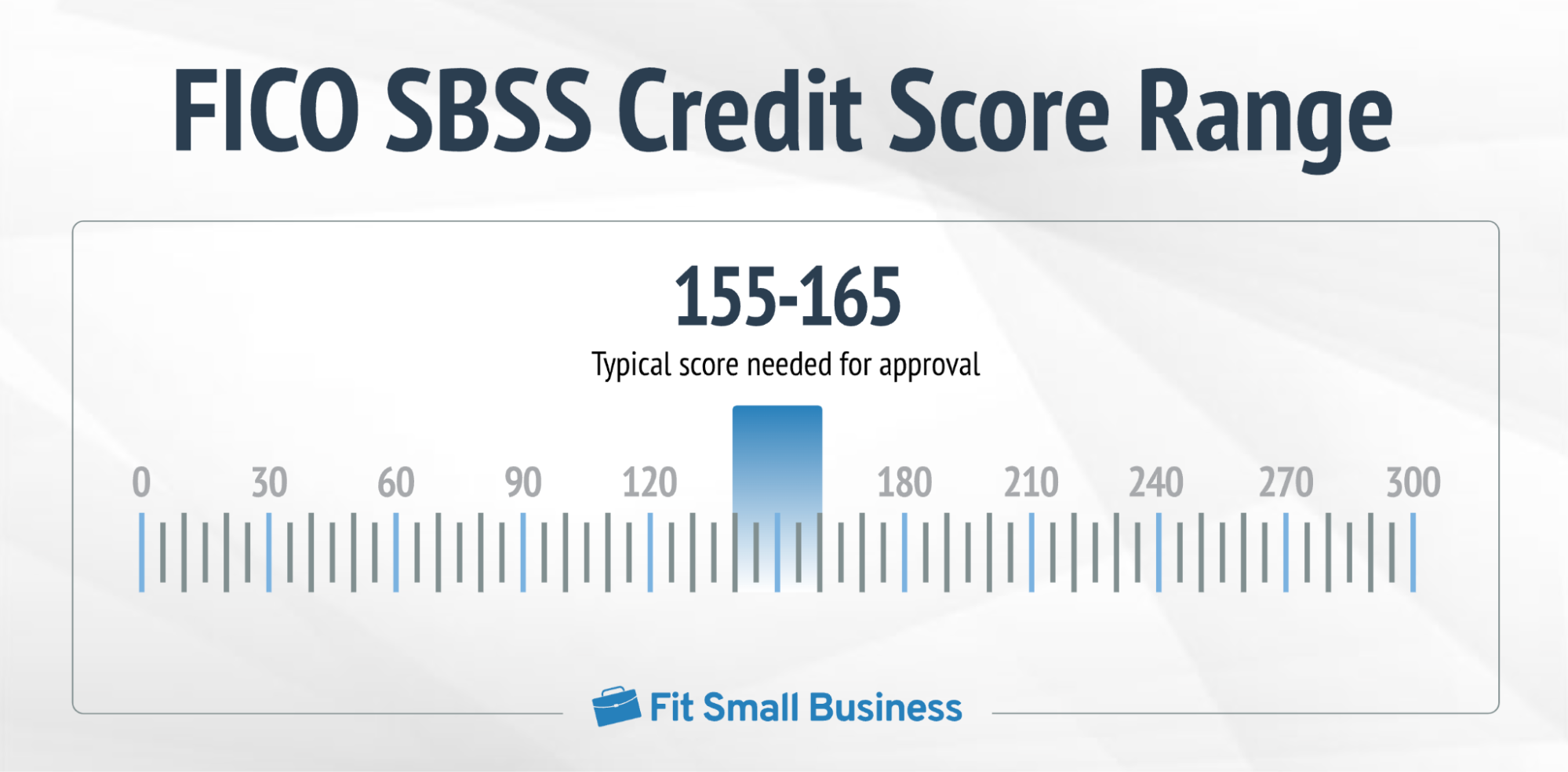

Although not universally required, a business credit score can influence your eligibility for a small business loan. One key provider widely used in the USA is the FICO Small Business Scoring Service (SBSS).

SBSS scores range from 0 to 300, with higher scores indicating greater creditworthiness.

This score reflects factors like payment history, assets, revenue, and business tenure.

For instance, to qualify for small-amount SBA 7(a) loans, you will need a minimum SBSS score of 155. However, FICO SBSS is just one of several scoring systems; others include Dun & Bradstreet, Equifax, and Experian. Lenders might consider these alternative scores when reviewing your loan application.

Most lenders require that a business has been operational for at least two years to qualify for a loan. This history shows you have experience managing a business and surviving initial challenges.

Your business’s annual revenue helps lenders assess your loan repayment ability.

Requirements typically vary from lender to lender, but generally, a minimum of $100,000 in annual revenue is necessary.

Additionally, lenders often look at the consistency and sources of your revenue. A steady upward trend can demonstrate your business’s scalability, potentially qualifying you for better terms.

It’s also important to differentiate between recurring revenue and one-time gains, as stable, recurring revenue might be more favorably viewed than sporadic income.

Some loans require collateral, such as real estate or equipment, which can be seized if the loan isn’t repaid. Alternatively, lenders might require a personal guarantee, which holds you liable if your business can’t repay the loan.

Billdu is more than just invoicing! Explore our advanced features and take control of your finances—try Billdu today!

Applying for a business loan involves several detailed steps, from drafting a comprehensive business plan to choosing the right lender. Here’s a step-by-step guide to navigating this process effectively:

You need a coherent business plan to demonstrate your business’s viability and success potential. Here’s a checklist of the primary things that you’ll need to include in your business plan:

You can utilize process mapping tools here to outline your business operations, which can further help clarify your business model and operational efficiency. These tools visually represent your business processes and make it easier to identify critical aspects that will make a case in front of the lenders.

Accurate and complete financial documentation is essential for lenders to assess your business’s health and profitability. This includes documents like:

Prepare to provide at least the last two years of income statements and balance sheets. These documents should clearly show your revenue, costs, and profitability and a snapshot of your company’s assets, liabilities, and equity at each year-end.

You must also provide business tax returns for the last two to three years, confirming your reported income and tax compliance. Monthly bank statements for the previous 12 months are typically requested to examine the business’s cash flow—lenders use these to verify the income recorded on other documents and to observe your company’s spending behavior.

Selecting a lender involves comparing different types of financial institutions and their offerings. You need to consider the interest rates, loan terms, and fees to determine the best fit for your business needs. Here’s a quick comparison of the options you may have:

When you’re considering a business loan, it’s crucial to grasp the terms and conditions attached to your potential borrowing. These elements dictate how much you’ll pay back and the flexibility and constraints of your funding. Let’s break down the key components:

Understanding how interest rates and associated fees work is fundamental in evaluating loan costs. Two common terms are Annual Percentage Rate (APR) and Interest rate.

The Annual Percentage Rate (APR) encompasses the interest rate and other associated fees. This makes APR a more comprehensive measure of the loan’s cost.

Loans often include various fees that add to the total cost of your loan, impacting the overall financial commitment. This includes:

Repayment schedules are a fundamental aspect of any loan agreement, directly affecting your business’s day-to-day financial management and the total cost over the life of the loan. Let’s get into the details:

The frequency of your loan payments can significantly affect your budgeting and financial planning. Monthly payments are standard and may align better with businesses with a traditional monthly revenue cycle.

On the other hand, weekly payments can be advantageous for businesses with consistent cash flow throughout the month, as these can reduce the total interest paid over time by decreasing the principal balance more quickly.

While paying off a loan early can seem appealing as it reduces the interest you pay, it’s essential to consider any early repayment penalties that might be in place.

These penalties are imposed by lenders to offset the lost interest income when a loan is paid off before the end of its term. Hence, before making extra payments or paying off a loan early, you must review your loan agreement for any mention of these penalties.

Once your business loan is approved, the journey towards managing the funds and repayments begins. Here’s a step-by-step breakdown of the post-approval process to help you navigate what comes next.

The first step after your loan approval is to review the loan agreement thoroughly. All of your loan’s terms and conditions, including the interest rate, repayment plan, costs, and penalties, are described in this document.

Once the loan agreement is signed, the lender will disburse the funds to your business account. The timing of this process can vary, but typically, funds are released quickly following the completion of all administrative procedures.

Managing your loan repayments effectively is crucial to maintain good financial health and credit standing. Mark your calendar with all due dates for repayments and prepare in advance to ensure funds are available to meet these obligations.

Setting up automated payments from your business bank account can be a wise choice to avoid late payments and potential penalties. Automating this process ensures that payments are made on time every month without fail, which also helps maintain a good credit score.

Keep a diligent record of each payment and invoices and the remaining balance. Monitoring your repayment progress not only helps you stay on top of your financial obligations but also allows you to assess the impact of the loan on your business finances over time. You can also utilize financial management software or simple spreadsheets to track and plan your finances efficiently.

Effectively managing a business loan is crucial for maintaining your company’s financial health and ensuring future access to funding. Here are some essential tips to help you manage your business loans successfully:

Always make your loan payments on time to keep your credit score healthy and avoid penalties. Consider setting up automatic payments to eliminate the risk of forgetting a due date, which can also simplify your financial management.

Keep records of all your financial transactions, including receipts, loan payment histories, and cash flow statements. Well-organized financial records not only help you keep track of your financial health but also prepare you for any audits or financial reviews.

Establish and maintain open lines of communication with your lender. If you foresee challenges in upcoming payments or are considering significant business changes, discussing these with your lender can lead to adjustments in your repayment terms.

If your cash flow allows, consider strategies for early loan repayment, which can save you money on interest in the long run. Review your loan agreement for any prepayment terms or penalties. Sometimes, making larger or extra payments during profitable periods can significantly decrease the interest accrued and shorten the loan’s term.

Understanding and managing business loans effectively is crucial for leveraging them to your business’s advantage. From choosing the right type of loan and lender to meticulously preparing your loan application and managing repayments, every step is significant.

Ensure you maintain good financial records, communicate openly with your lender, and consider early repayment strategies when feasible. By staying informed and proactive about your business financing, you can not only meet your current financial needs but also position your business for future growth and stability.

Get a comprehensive view of your finances with the Billdu app. Check our pricing today to start managing your finances effectively!

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy